By Eyamu Jimizani

Uganda Secures Over $2 Billion in World Bank Financing to Bolster Development.

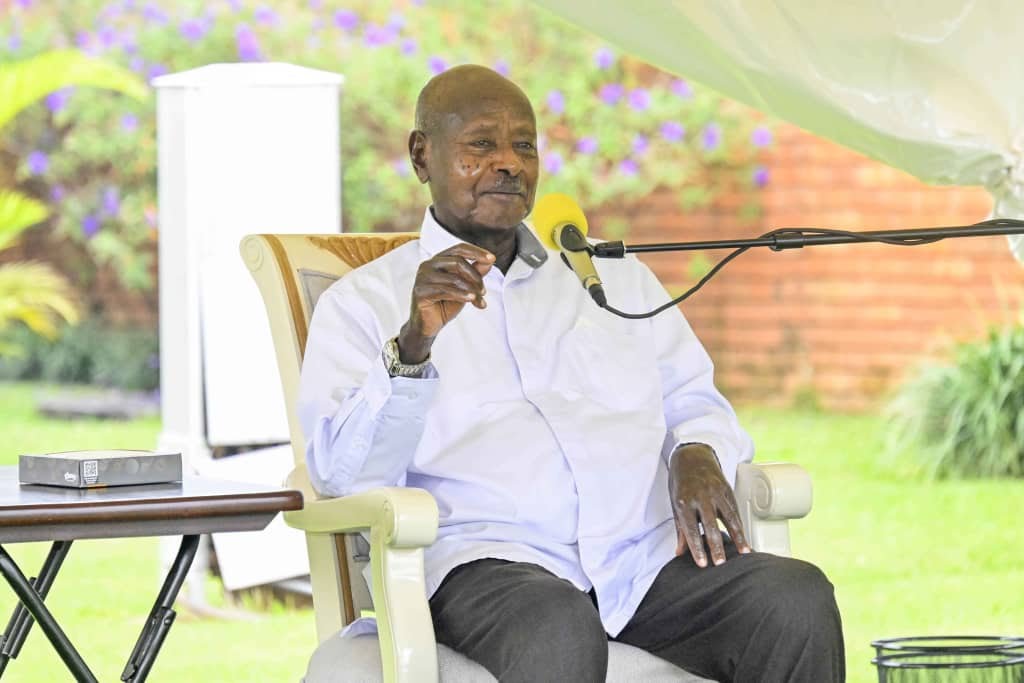

Uganda Secures Over $2 Billion in World Bank Financing to Bolster DevelopmentKampala, Uganda – October 23, 2025 – Uganda is poised to receive more than $2 billion in concessional financing from the World Bank over the next three financial years, a move set to advance the nation’s development priorities across critical sectors. The announcement was made by Ramathan Ggoobi, Permanent Secretary and Secretary to the Treasury, following the successful conclusion of the 2025 IMF and World Bank Annual Meetings in Washington, D. C. The new funding increases Uganda’s total investment portfolio with the World Bank to $4.9 billion. According to Ggoobi, the resources will support key areas, including road and bridge infrastructure, electricity transmission and distribution, urban development, education, information technology, agriculture, water and irrigation systems, export guarantee programs, skills development, and social protection initiatives. Ggoobi highlighted a strategic shift in the World Bank’s approach under President Ajay Banga, emphasizing private sector empowerment to drive job creation and economic growth. The International Finance Corporation (IFC), the World Bank Group’s private sector arm, will support these efforts by providing long-term capital for investments in minerals, renewable energy, agro-industrialization, and innovation, alongside facilitating public-private partnerships in select state-owned enterprises. In parallel, Ggoobi confirmed ongoing negotiations with the International Monetary Fund (IMF) for a new Extended Credit Facility (ECF) program, expected to commence following Uganda’s national elections. The program will focus on enhancing domestic revenue mobilization, maintaining budget discipline, and strengthening the financial sector to ensure sustainable economic growth. Both the World Bank and IMF have praised Uganda’s economic resilience and prudent macroeconomic management. The IMF ranks Uganda among Africa’s fastest-growing economies, attributing its success to sound fiscal policies and a dynamic private sector.“The World Bank’s commitment aligns with Uganda’s tenfold growth strategy, particularly through investments in technology and its enablers,” Ggoobi stated, underscoring the government’s dedication to fostering stability and prosperity.

Go Back to All Posts

Trending Now - TOP 100

1

Why Africa’s Mineral-Rich Countries Stay Poor: The Hidden Truth Behind Cobalt, Gold, and the Resource Curse, and Profit Shifting.

2

Crystal Palace stunned Liverpool to win the Community Shield

3

More than 50k Russian troops have deserted war from Ukraine

4

Michelle Obama Says America “Ain’t Ready” for a Woman President: Candid Remarks on Kamala Harris Loss and Gender Bias in 2025.

5

MIT Study Reveals AI's Fatal Flaw: Why ChatGPT Still Can't Understand 'No.

6

Why Your Phone Screen Is Shaking: Causes, Fixes, and Prevention Tips

7

Introducing Runfarbiz Network TV Global News software 2026

8

Jeff Bezos Reclaims No. 3 Richest Title From Sergey Brin After Amazon Store Closures

9

Best Music Affiliate Program This 2026 For Musicians.

10

Germany's Air Power Pivot: Inside the 20 New Eurofighter Typhoon Order

11

Elon Musks SpaceX to invest in xAI From $2 billion funding to $113 billion valuation.

12

Niki Biography And Music – Indonesian Singer-Songwriter, Global Pop R&B Artist, Career and Music Journey

13

Aliko Dangote Became The Richest Black Man In The World — And Now He Plans To Invest $1B In Industrial Projects In Zimbabwe.

14

Kampala Traffic Jam Continues To Be Dominated By Bodaboda Riders & Taxis Amidst Coming Events.

15

Acidic Vokoz plans another major concert

16

ARSENAL TO SIGN MADUEKE FROM CHELSEA

17

WordPress Settings Required For Any Good Website Development And Clean User Interface

18

Types of Hacking Methods That Are Popularly Being Used By Hackers.

19

Man United receive key Marcus Rashford transfer exit 'approval' as £44.8m enquiry made

20

SPORTS: All transfer rumors

21

The health benefits of eating sugarcane on daily basis

22

YOU CAN CONTACT SYPHILIS IN YOUR EYES IF YOU ENGAGE IN THESE THREE THINGS.

23

Ugandans spend Shs 55bn a day on TikTok data - Report

24

What Is Agood Webhosting ?

25

Do These Simple Steps To Stop Mustarbation Addiction.

26

Kalaki Leaders Embark On Benchmarking Tour To Revive Education Standards At Top-Performing VH Public School

27

UPDF has disqualified More than 60000 Applicants In Intitail Phase Screening.

28

Tulus Biography Details And Music Of The Artist

29

Fintechs Dominate Africa's Top Startup Valuations in 2025: Flutterwave, OPay, and Wave Lead the Unicorn List.

30

Runfarbiz Related Premium Offers Now Includes Investment, Subscription For Voice, Data & Airtime Bundles Options Updated.

31

We are now operating on both Ads revenue Model and Subscription Offers Just like Spotify, TikTok, Deezer, Apple Music , Mdundo, Boomplay, YouTube Music, Facebook Streams , Latest Runfarbiz Network system Upgrade.

32

Crazy Things Awife May Do To Mess Up Her Relationship

33

Solomon Kampala, Son of Bobi Wine, Engages Mexican Partner Helen Jaquez in Stunning Lakeside Proposal

34

Africa aviation industry, Isaac Balami University of Aeronautics and Management, IBUAM, first aeronautics university Africa.

35

Iran holds state funeral for military leaders killed in Israel conflict.

36

Protect your soul, The world isn’t worth it.

37

Billionaires Elon Musk and Mark Zuckerberg almost ended up in a cage fight over their competing social media platforms.

38

NRM Party Primary Elections Has Failed UpTo Ten Ministers , Report Confirmed by Electoral Commission Uganda.

39

A comprehensive biography of Raila Odinga, exploring his journey from political detainee to Prime Minister, his five presidential bids, and his complex legacy in shaping modern Kenya.

40

The tech world was left stunned when Perplexity, the $18 billion AI startup led by Indian-origin CEO Aravind Srinivas, made an audacious $34.5 billion cash offer to acquire Google Chrome.

41

Nigerian researcher develops wireless charging tech for electric vehicles.

42

Official Digital Transformation Update From Runfarbiz Network Admin, Try To Read To The Last Paragraph

43

Two Suspected Ugandan Rebels Killed in Kampala Explosion.

44

Billionaire Telegram Founder Leaves His $14 Billion Fortune to the 100+ Children He’s Fathered—Which Means $132 Million for Each Lucky Gen Alpha Kid.

45

Trump Health 2025 Perfect MRI No Idea What Body Part Was Scanned, Full Story.

46

The landscape of modern warfare is on the brink of a seismic shift, and China is at the forefront of this transformation.

47

Uganda Secures Over $2 Billion in World Bank Financing to Bolster Development.

48

_biography_–_the_rising_star_in_the_music_industry..jpeg)

DAX (Daniel Nwosu) Biography – The Rising Star in the Music Industry.

49

Assistant referee Peter Kabugo passes away during sports club Villa match against UPDF

50

The Opposition Claims Hundreds Of Tanzanian Protesters Around 700 Already Dead.

51

Uganda Police Ban Campaign Processions and Ambulance Misuse as Bobi Wine Launches Kampala Campaigns in Kawempe | 2026 Elections.

52

Exposed Tricks How Some Financial Credit Institutions In The Names Of Money Lenders Are Stealing From Poor Ugandans .

53

Qatar, UAE, Saudi Arabia, and other Gulf nations have shut down airspace amid rising tensions, causing massive flight cancellations and travel chaos. Latest updates here.

54

Uganda’s New Law Allowing Military Trials for Civilians.

55

Russia Begins Production of Advanced Oreshnik ICBM: A New Era in Strategic Capabilities.

56

Iran-Israel War: Origins, Casualties, Global Impact, and Future Projections.

57

Why J Donald Trump Is Still Dominating American Politics

58

Daily USSD Codes for MTN UG and Airtel UG that may assist you when having some Emergencies.

59

Mdundo Temporarily Blocked My Music Page After Hitting 1 million Streams Plus, My 5 million Uganda Shillings Will be losts .

60

SEE NAMES OF UGANDANS SHORTLISTED FOR GOVERNMENT PAYROLL JOBS AS HEAD TEACHERS, DEPUTIES IN KCCA SCHOOLS.

61

Six Dangerous Diseases You Can Catch Through Kissing _What You Need To Know.

62

TotalEnergies Sued in Uganda Over Unpaid Bill for Toxic Fuel Depot Cleanup in Kampala.

63

Top Most Corrupt Institutions Made To Control Human Race Under The Financial Matrixs They Are Not Telling You.

64

UPDF Bids Farewell to Over 600 Retirees in Nationwide Ceremonies.

65

UGANDA SIGNS BILATERAL AIR SERVICE AGREEMENT WITH OMAN.

66

Runfarbiz Network Improved Streaming Features Includes The Following.

67

Microsoft has unveiled their new Copilot AI model

68

VINKA AND FIK FAMAICA TO LEAD MUBs GALA

69

Uganda and Kenya Assure No War Over Indian Ocean Oil Dispute , Museveni Remarks, Mudavadi Response & EAC Diplomacy 2025.

70

See why your always having sex on dreams, Secrets Exposed.

71

The Secret Life of Squirrels: A Tale of Love, Loyalty, and Forests in the Making.

72

President Yoweri Museveni has promised to address two critical needs in Obongi District—electricity and better roads

73

Antoine Semenyo £65m Release Clause Active in January: Man City, Liverpool & Spurs Monitoring Bournemouth Star.

74

Singer Daudi Mugema dies in Gulu

75

Bebe Cool Announces Release of New Single, ‘Circumference’

76

REPORT REVEALS ALARMING HUMAN RIGHT ABUSES IN KARAMOJA MINING SECTOR.

77

SFC soldier shoots three dead in Agago

78

Uganda and Kenya Harmonise SGR Standards: Land Acquisition Accelerates for Malaba-Kampala Railway Project.

79

Auditor-General Demands Shs2 Trillion Forensic Tax Audit on Uganda Telecom Companies Over Revenue Discrepancies.

80

Arsenal Eye Move for Liverpool Wonderkid Joshua Abe | 15-Year-Old Right-Back Transfer News.

81

British firm discovers gold worth over $5B in western Kenya.

82

U.S. President Donald Trump recently expressed admiration for Pakistan.

83

CDF Kainerugaba On Behalf Of UPDF Is Planning To Reshuffle Their Generals Like GEN Elwelu.

84

GOVERNMENT OF UGANDA TO RECRUIT OVER 2800 TEACHERS AHEAD OF NEW TERM.

85

UPC's Jimmy Akena Vows No Space for NRM in 2026 Elections: Uganda People's Congress Resurgence Ahead of General Polls.

86

Bunyoro Kingdom Rejects UCDA Rationalization, Calls for Increased Funding

87

H.E Yoweri Kaguta Museveni Is The Most Concerned Ugandan Patriot.

88

25 Motivational Tips & Quotes that shall Inspire You.

89

Kylian Mbappé Breaks Messi Record: Youngest to 400 Career Goals Since Pelé at Age 26.

90

Why Bobiwine Has Been Failing The Political Presidential Elections In Uganda.

91

Pakistan Tightens Cash Dollar Sales in Bid to Curb Outflow and Support Rupee.

92

4 THINGS MOSQUITOS DON'T LIKE, WHICH WILL MAKE THEM RUN FROM BITTING YOU.

93

How to stay the happy life without money in your pocket

94

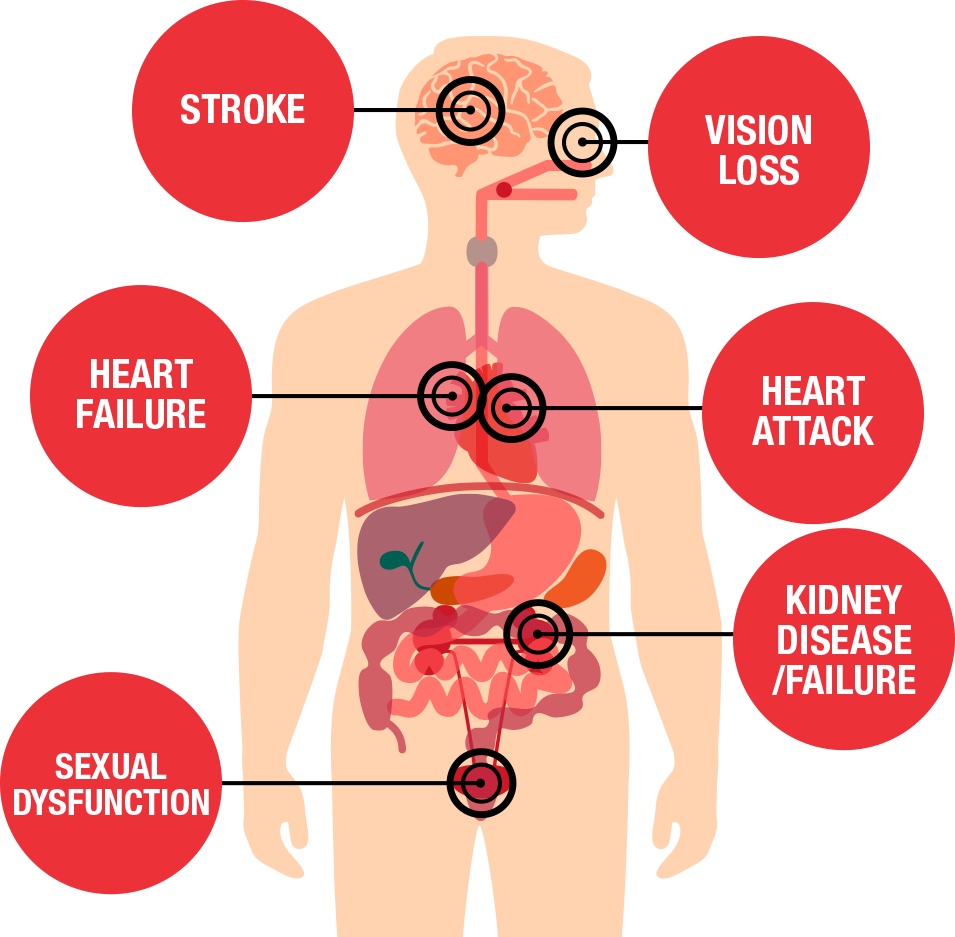

Causes and prevention of high blood pressure

95

Stop praying like this, You will summon demonic forces from abyss without knowing

96

Boywisky music official ft Bill Ranka Uganda have already released a new song titled "Yom Cwinya"

97

In tit-for-tat, Zambia suspends Kenya Airways flights over country’s denial of access to Zambia Airways

98

HOW UGANDAN'S ENERGY SECTOR WILL PERFORM IN 2026.HOW UGANDAN'S ENERGY SECTOR WILL PERFORM IN 2026.

99

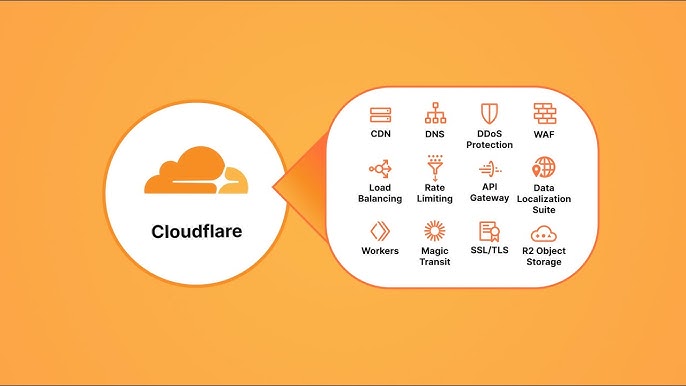

Cloudflare Outage November 18 2025: Why the Internet Broke and How Cloudflare Actually Works Behind the Scenes.

100

UPDF SALUTS SEVEN GENERALS , AWAITING THEIR OFFICIAL RETIREMENT

RECENT CONTENTS

Goyo hustle by FreshBoy dabless rapper ft vanny kanotty_-_Asassin Skylord is out

FreshBoy Dabless, alongside rising artists Vanny Kanotty and Assassin Skylord, has officially released a brand-new hit titled “Goyo Hustle.” The track delivers a powerful message centered on determination, hard work, and the everyday grind for success. “Goyo Hustle,” which translates to hustling, reflects the artists’ real-life experiences and ambitions in the music industry. The collaboration showcases unique styles, energetic delivery, and a strong connection to street culture. Fans and music...

Read More

Biography Of The Chainsmokers

The Chainsmokers are an American electronic music duo comprised of Alex Pall, born on May 16, 1985, and Drew Taggart, born on December 31, 1989. The two came together in New York City in 2012 after Alex, who had been working as a DJ, was introduced to Drew through a manager. They quickly bonded over their shared passion for dance music and began producing original tracks and remixes, initially gaining...

Read More

Irans Supreme Leader Confirmed Killed By Israels Joint Attack With America

On February 28 and into March 1, 2026, Israel and the United States launched a coordinated joint military operation against Iran, marking a significant escalation in long-running tensions over Tehran’s nuclear and missile programs. The offensive involved extensive airstrikes by Israeli forces and participation by U.S. military assets targeting Iranian military infrastructure, command centers, missile sites, air defenses, and political leadership compounds. Several senior Iranian officials and commanders were reported...

Read More

WestLife - Biography And Their Music Journey.

Westlife, the Irish pop group, came together in Dublin in July 1998 when Shane Filan, Kian Egan, and Mark Feehily, who had been schoolmates from Sligo, joined forces with Nicky Byrne and Brian McFadden following auditions to complete the original five-member lineup. by Louis Walsh and initially supported by Ronan Keating, they quickly signed a >

Managedajor record deal and burst onto the scene in 1999 with their debut single...

Read More

Niki Biography And Music – Indonesian Singer-Songwriter, Global Pop R&B Artist, Career and Music Journey

Nicole Zefanya, known professionally as Niki, is an Indonesian singer-songwriter born on January 24, 1999, in Jakarta, Indonesia. She is recognized for her alternative pop and R&B sound and is signed to the record label 88rising. Over the years, she has gained global recognition for her songwriting and musicianship, building an international audience while living and working in the United States.

Niki began developing her musical skills at a young age...

Read More

Afgan Music And Biography Of The Artist – Indonesian Singer, R&B Artist, Albums, Career Journey, and Music Evolution.

Afgansyah Reza, known professionally as Afgan, is an Indonesian singer and actor born on May 27, 1989, in Jakarta, Indonesia. He is widely recognized for his smooth pop and R&B style and has become one of Indonesia’s most prominent contemporary male vocalists.

He grew up in a musical Muslim family of Minangkabau heritage and is the second of four children.

Interestingly, despite later becoming famous for his voice, he never underwent...

Read More